$BLND: A Primer and Idea

Vitamix or Chinese knock-off?

Intro:

This article will hopefully be one of many where I discuss interesting ideas. The depth of said articles will likely vary, with some being more surface level and some being more deep dives. The goal is to both get myself looking at a minimum of 1 thing a week as well as sharing thoughts. Writing also helps to condense ideas, so we can call it mutually beneficial.

Currently I have no plans to paywall these weekly write ups, but that may change, or maybe only paywall full theses. I do appreciate all subscribers and hopefully a subscription (free or premium) is worth your while. If that excellent sales pitch piqued your interest, feel free to do so below.

The topic of this weeks post is Blend Labs, aka BLND, a ~$285m market cap company that went public in 2021. BLND essentially provides mortgage origination software for banks (collecting info and such from consumers faster than a human/in house code solution). The share price has quite obviously cratered since going public, now trading at a touch over $1, down ~95% in 2 years. Astute readers may be aware of some extenuating circumstances during the 2021-2023 time period that perhaps influenced mortgage markets.

I do currently own a position in my PA, however it is rather small at a few % of capital. Given my penchant for concentration hopefully this article can explain why I believe BLND is interesting and also why it is sized as such. I avoid getting too in-depth with financials, mostly focusing on the story and key questions.

Banks and the 21st Century:

Before touching more on BLND, I find it important to discuss why this business may even conceptually be interesting, which requires us to start with banks.

The fascinating thing about banks is that almost everyone has one, or maybe even two or three. Banks have all of your personal information, they know what you buy, what you make, what you wear, etc. They sit on a certified treasure trove of consumer information and data and you are forced to interact with them for what is generally no value to you besides holding your money safer than a mattress and the occasional loan.

Unfortunately for banks, banking is quite hard. The best of banks might make a ROE vaguely similar to market returns while under quite a bit of leverage. This output is the result of the focused labor of thousands of individuals working under the constraints of thousands of pages of regulations. This leaves little room for nuisances such as “technology” and “data science”, or if there is room the amount of red tape on any endeavor mixed with the juggling of thousands of priorities causes some headaches.

Essenetially what I’m saying is that despite the absolute treasure trove at their finger tips, banks don’t tend to execute well on tech. I also believe said issue is structural given the plethora of regulations in the space and other focuses required to run a bank. The general rule of thumb is that banks prefer to buy instead of build, but are also very willing to buy if it makes the rest of their lives easier. The money must flow after all.

The specific part of banking we’ll be focusing on today is the mortgage origination side. If you’ve never had the joy of filling out a mortgage application, it’s a rather boring process. You fill out your personal information such as name, occupation, income, etc. Once said form is sent to a bank they do a nice little review to verify your information isn’t fraudulent and put the info into an algorithm to figure out if you qualify. All of the difficulty is abstracted away by 5 Indian guys and a data science team you’ve never heard of.

Sounds simple enough. The thing is though that mortgages tend to be a game of inches. Doing just a little bit better at fraud protection, just a little bit better at efficiency, just a little bit better at underwriting. Unfortunately, again banks aren’t all that great at tech. Some things that would help the aforementioned 5 Indian guys and data science team would be info that can be hard to get and verify from customers. Linking and verifying assets, automating away any chance for the paperwork middlemen to make a mistake, automatic database checking for fraud, etc. There are a bunch of potential boxes to check and not a lot of engineering talent to swing at them. Issues can pop up with lost paper work or the like and then there’s a headache and a whole lot of friction, which tends to be bad for closing rates.

This is where Blend comes in. Blend effectively acts as a plug and play SaaS for banks looking to streamline their mortgage origination process. Instead of designing your own customer facing origination forms, linking it up with your loan officers on the back end, linking it up with your decision engines, and hoping all of the machine and human inputs work out correctly, you wash your hands of it and plug in some API calls. API calls also tend to be a touch less expensive than having a loan officer spend his day realizing he forgot some paperwork, calling a customer that spends 30 minutes finding their pay stubs, they don’t know how to email a picture, so they’ll drop it off next week, etc.

In short, BLND does a mix of both improving revenue and reducing costs. They deliver a neat polished front end consumer experience will all the up to date bells and whistles like follow up texts and non-shitty UI’s. They deliver a back-end to reduce labor input requirements and optimize decision making with standardized data inputs and account linking.

Rather unsurprisingly, this abstraction away of human interference saves quite a bit of money. Blend quotes it in the realm of ~$900 of ROI from labor savings/time savings/tech savings for each mortgage loan. This is due to the dozens of manual touches required for each loan origination that can simply be abstracted away with technology. I would note that this number is somewhat arbitrary. There are >4,000 banks in the US and not all of them have engineering weight to even attempt to recreate what Blend does, but there are quite a few that do. JPM for example I doubt would ever be a Blend client, and the customer base is largely smaller banks. They do however have US Bank and WFC as clients, which speaks to the value of the platform.

Personally I take everything with a grain of salt, so further testing is necessary to believe in the value proposition. A basic thought experiment would be as follows:

If BLND provides positive utility to firms, market share should increase over time.

Labor is somewhat less flexible than the overall mortgage market. Upsizing and downsizing proactively is difficult if not impossible, meaning its possible to be over or understaffed frequently.

If BLND can provide costs based on variable mortgage volumes while drastically reducing touches from human employees, then in theory BLND should be very valuable during periods of rapidly declining mortgage volumes to get expenses in line.

Thankfully this is a testable idea, and one that BLND provides some info on.

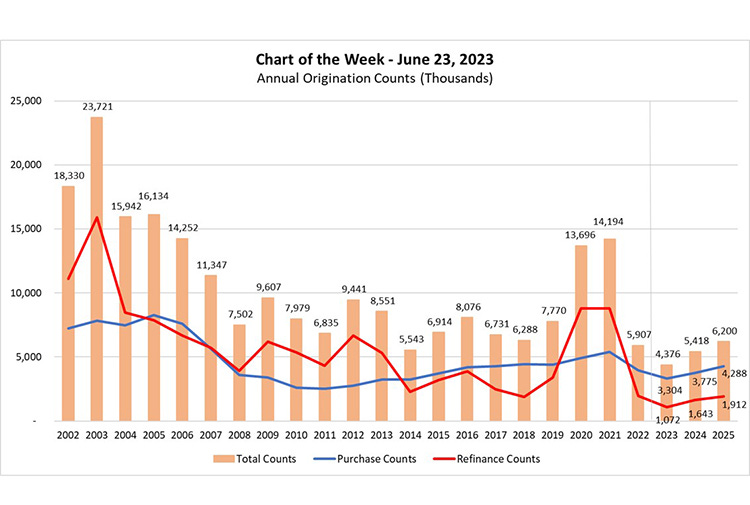

First off, a chart of how mortgage volumes have trended over time.

Second, some BLND provided data, per BLND’s Q1 2023 earnings release:

“Continued Market Share Gains: Blend’s mortgage banking software processed 23.2% of the total market originations as measured by the Mortgage Bankers Association in the second half of 2022, up from 14.5% in the second half of 2021.”

So essentially, BLND rockets into prominence during a drastic spike in refinances given rate policy, then takes significant share in 2022 as the industry collapses in on itself. This is somewhat intriguing, as while revenue of course collapsed from the significant drop in volumes, banks clearly indicated a strong preference for digitalization and a more economic model, proving that BLND provides significant customer value throughout the cycle.

Hopefully this is rather convincing data to the point that banks need BLND or something like BLND versus how things were traditionally handled with shoddy in-house engineering or high amounts of manual labor. The key question remaining of course would then be, why BLND specifically?

Why BLND Specifically

First off, just conceptually, making tech for banks is a PITA. Regulatory and security requirements mean it isn’t something you just spin up randomly. This doesn’t prevent competition, but it does limit the pool.

Additionally, banks are big fans of rapid change if that isn’t obvious by now. Ripping out BLND for another provider isn’t something that happens overnight.

Lastly, I doubt mortgage origination is a sexy place to be on either side of the isle currently. For banks, there are likely business segments demanding a bit more attention than trying to optimize volume in a dead market, similar to what we’ve seen with pullbacks in auto lending. For tech companies, it’s all AI blah blah, probably not going to see any big rate asset related IPO’s any time soon given market dynamics. BLND is down about 95% over the last 2 years after all, not exactly and industry screaming for capital and attention.

As a result, BLND doesn’t have much direct competition currently. Alternatives such as Roostify, SimpleNexus, and CloudVirga are all drastically smaller, like more than 10x smaller, all of them combined a fraction of BLND’s size types of smaller. Roostify was taken private earlier this year, likely at an atrocious valuation given market dynamics, and across the board all have seen significant spending cuts, shedding >50% of employees in 2022 in some cases.

Of course this doesn’t mean that BLND will always win, and it’s always possible other entrants can introduce a better offering, however that isn’t particularly relevant to this thesis over a 2-3 year time horizon given the slow moving nature of banks and the headache associated with vendor replacement. Additionally the way the stock is priced is a heavy influence, with uncertainty regarding solvency in 2-3 years, yet alone forward competitive position.

So to summarize where we are at currently:

Banks clearly value digital origination vendors given significant market share gains at BLND over the past few years

There is no meaningful competition to BLND in the next 2-3 years

The obvious question of course, if the above is true, why is the stock down 95% since IPO?

Why BLND (the stock) Specifically

As always, I find it key to figure out WHY the stock has been shit before assigning any judgement.

To start, we can simply take a look at the IPO date, Q2 of 2021. At point in time at which the Nasdaq had doubled in the last 15 months, and saw pictures of monkeys selling for hundreds of thousands of dollars. Just for fun, lets look at some price action amongst BLND’s SaaS 2021 IPO cohort

MNDY: -13%

CFLT: -27%

GTLB: -56%

S: -63%

TOST: -63%

Many of these companies are sporting revenues more than double what they were in 2021, while also seeing their stocks get absolutely killed.

Obviously BLND at -95% is an outlier in a bad way, but timing and general market movement makes it a bit impossible to have a pretty story over the past 2 years.

To be brief, BLND also saw a couple of their own hiccups:

They deal with mortgage originations, which tanked as seen above

They acquired Title365 for $422 million in early 2021, more than their current market cap of $285 million.

Title365 acquistion was essentially a flop and much had to be cut as originations torpedo’d in 2022.

They have out standing debt slightly lower than their current market cap while also having negative EBITDA in the TTM.

Mortgage markets are inherent unpredictable and rates are much higher currently with no clear sign of easing, so refinances may be quite weak for the foreseeable future.

The key here being #4 and #5. It is uncertain if BLND can cover their future debt obligations and uncertain if they can become profitable before those are due. This is the key question that needs to be answered.

There are a few variables that will play into answering said question

What are mortgage origination volumes?

What is BLND’s market share in 2-3 years?

How much can BLND earn per mortgage origination?

How much will it cost BLND to run the business

(As an aside, there is also the title business. This business has a large chunk of BLND’s revenue, but effectively doesn’t contribute to margins at the end of the day, so it is left out of this exercise)

Unfortunately, I don’t have a great answer to question 1. Hiccup number 5 above is an undeniable fact of life. BLND can gain market share as much as they like, but if refinance volumes are in the toilet for the next couple years, that’s a rather large headwind. CVNA or CDLX as an example have drastically lower market share than 23%, so I had higher conviction in their ability to maneuver around some self inflicted pain. Call BLND suffering from success.

As for question 2, I’m going to take a wild guess that BLND will continue to take share given the value provided to customers in a tough environment and the secular trend towards digitalization within bank channels. I would be surprised if BLND cannot surpass 25-30% share in the next 2-3 years.

For question 3, some basic math spits out maybe $90-100 per transaction (take volume, assume a share, calculate with BLND’s reported mortgage revenue). Given reported savings in the realm of $800-900, there is likely some room to increase BLND’s take rate. This has happened over the course of 2023 as they’ve - had revenue perform better than market volumes.

Per the 2Q2023 report: Within the Platform segment, Mortgage Banking Suite revenue declined by 17% year-over-year, to $22.3 million, amidst a 37% mortgage market volume decline over the same period as reported by the Mortgage Bankers Association.

Per the 1Q2023 report: Within the Platform segment, Mortgage Banking Suite revenue declined by 33% year-over-year, to $17.8 million, amidst a 58% mortgage market volume decline over the same period as reported by the Mortgage Bankers Association.

Sadly there was a disclosure change starting in 2023 that makes it hard, but similar rough math as above would indicate maybe $70-80 per transaction in 2H21 versus the $90-100 currently, indicating BLND is taking price.

How much price can be taken is of course up to the reader, but if we assume say $120 or so over the next couple of years, that sounds vaguely reasonable.

Per question 4, we likely will see costs bottom sometime in the next couple of quarters as they’ve been cutting expense for awhile now and guidance is starting to imply losses are levelling out in Q3 amidst vaguely similar revenue. One could argue the guide is conservative, but the current expense run rate is likely around where they’ll be.

To put all of that into numbers and add some context (this is grossly over simplified and is intended as a mental exercise to directionally determine vaguely what is required, not an actual liquidity model)

BLND has around $250m of cash, with $225m of debt and is burning roughly $20m per quarter. If we assume 2023 ends as expected, they’ll be around $210m of cash.

Let’s go over our assumptions:

Assume mortgage volumes are roughly 12 million over 2024 and 2025 - this is assuming a rebound to slightly above 2022 levels as rates stabilize. A big wild card most certainly and very hard to pin down

Assume 30% market share on average for those 12 million originations

Assume $110 revenue earned on average per origination

Assume OpEx stays relatively flat from Q2/Q3, as well as interest expense. (Interest income would decline as cash goes down most likely).

Thus over 2 years BLND would see about $400m in mortgage origination revenue, roughly $50m per quarter. Given they’re at the low 20’s currently, that is a significant bump. The largest driver is origination volumes, which would be up over 50% from current levels. Taking price would drive 10-20% growth, and market share gains would drive ~30% growth.

Gross margins for that product would be >85%, implying about $185m or so of incremental gross profit dollars over 2 years, which is $23m per quarter.

Assuming they can continue to eek out another $10m of gross profit per quarter from their growing consumer banking and professional services, as well assigning a smidgeon of value to title, we’d be looing at maybe $30-40m of incremental GP dollars per quarter in 2 years. This would bring quarterly cash change from -$20m to +$10-20m. Thus our yearly cash flow would be maybe $40-80m, which is plenty enough to refinance $225m of debt.

SBC is of course rather large here, but it’s non-cash and getting diluted is the least of your concerns if things don’t work out. If BLND can get to the point illustrated above, the future growth prospects are hopefully a tad brighter and SBC can be handwaved by future buyers. This framework is a bit messier than most would like, but tends to workout in my experience. Effectively the question isn’t what the business is worth in 2-3 years, it’s what the business is worth to someone else in 4-6 years.

Of course the above contains a lot of assumptions. The revenue and market share assumptions are perhaps the most comfortable. BLND is clearly quite valuable and as a consequence has rapidly gained share while also expanding price.

The OpEx assumption is rather lazy, but I’d assume somewhat fair. We likely see OpEx lower in the near term as they get as lean as possible, then slightly expand throughout 2024 and 2025, with hiring limited to key functions. This is a rather standard playbook. Notably I don’t assume a ton of incremental OpEx for drastically higher revenue. This is simply a function of the product, wherein end consumer usage is rather detached from actual BLND execution. More engineers won’t make consumers buy more houses, and more consumers buying houses doesn’t require more engineers, simply more server cost.

Of course as mentioned, market total originations is just a massive wild card. If we dropped our 12 million originations in 2 years to 8 million, in line with 2023, the math implodes and you cut incremental GP in half or worse. The question then becomes can you start rapidly pushing price while also rapidly expanding market share? It just makes things far harder for BLND to execute on and harder to believe in incrementally.

The other GP lines I hand wave are harder to build out an easy model for. Intuitively the more successful and intertwined the mortgage business is, the better everything else will be. The title segment will likely be rather worthless, but spit off a tiny bit of cash as they leverage volumes. The consumer banking initiative has been growing, but it’s nothing sexy that will save the day, maybe just spit out an additional LSD-MSD millions. An exact number is going to be up in the air, but the main question will remain the mortgage side.

As such I have BLND at a LSD-MSD % of my portfolio. The uncertainity of the largest driver is very hard to be comfortable with, but the opportunity seems rather asymmetric. Your floor price here likely isn’t $0 given the extreme market share. If things don’t work out I wouldn’t be surprised if they get bought out lower. You might take a 50-70% haircut, but better than -100%. The upside could be $3-4+ if they can get to spitting out a decent chunk of FCF with good future growth prospects. Worth a swing for me, by DYOR.

Some Worries:

Some additional worries.

Management is rather sparse. You effectively have the CEO Nima Ghamsari and not much else. This isn’t something like CVNA with a built out team weathering the storm together. IPO’ing when they did was clearly an excellent choice, the product is superb and clearly valuable, scaling has been great and market share gains and price taking has worked out well this year. On the flipside capital allocation was horrendous in 2021 (as were many other companies such as CDLX and CVNA…), the organization had to flip on a dime and fire a bunch of staff, the Title365 acquisition was not only poorly timed but potentially not even worth much. It’s a mixed bag. I’m willing to forgive 2021 capital allocation sins given movements since have made sense, but any hiccups in execution would be a cause for major concern.

Threading the needle of share growth and price taking can be hard. Customers can leave for totally random and irrational reasons. The margin of safety isn’t gigantic here if WFC and USB for example just decide to leave. By all accounts CDLX offers offer some of the best ROI in the ad market, yet SBUX and ABNB just up and left. This is a real risk for BLND where theory of stickiness doesn’t always match reality and is inherently unknowable.

The competitive landscape could change in 2-3 years, leaving BLND trying to compete against new comers with additional capital while saddled with significant debt. The barriers to entry here aren’t as high as say a multi-billion dollar CVNA infrastructure investment. They aren’t low by any means, but conceptually everything that BLND does isn’t hard to replicate technologically. Given returns are largely going to be based on growth potential beyond 2-3 years, we need the market to believe the business is solid in 4-6 years, so narrative violations would hurt.

Things to Track:

Going forward the KPI’s for BLND are roughly as follows:

Market share - We need this to expand

Revenue per transaction - We need this to expand

Gross margin - We need this to expand

OpEx - any unexplained jumps can torpedo the thesis.

If any of these points do not go as planned, it’s likely a narrative violation and indicates some part of the thesis logic is wrong. 2023 has fit the narrative above, but can never be certain that makes the narrative correct.

Fin:

Hopefully this was helpful to those potentially interested in BLND. I do not dive into abstract data sources and really get into the guts of how things work here, which is somewhat intentional. I personally find it hard to justify reconfirming hypotheses 3-5 times each for a position this small. This will naturally lead to lower conviction and higher likelihood of a mistake, so take that as you will. I am not responsible if you buy BLND and it doesn’t work out.

I may do a follow-up article at some point with more detailed numbers and the like, that will simply depend on how the opportunity develops.

Next week I plan to release an article with an update on high level thoughts of CDLX including why it continues to be my highest concentration position (now at ~60% of my PA). This may be redundant with Swany407 Investment Research if you are a subscriber of his, if not you likely should be. I will also spice up the specific name articles with more philosophy articles, similar to a typical HF letter as I am being inundated with 1H23 variants and might as well add some thoughts to the void.

Apologies for this one being slightly later than expected, real life has been throwing some curve balls recently that will likely continue for a smidge (including delivering a dozen antique rugs via U-Haul across the country, a man of many talents). I will try to follow the 1/week guidance, but will graciously ask for your flexibility.

If you would like to subscribe, feel free to do so as always.

Please consider contacting @AndrewRangeley about appearing on an episode of his yet Another Value Podcast to discuss $BLND & $CVNA:

https://www.youtube.com/@yetanothervaluepodcast

He profiles investors who have eclectic stock picks.

Great, thanks