Idea Overviews - Tickers and Thoughts

As promised, it’s late June (very late) and I have a weekend to go through some tickers I’ve been sent as well as some I’ve personally come across. The goal if this article is to be a shorter little primer on things, both to spread awareness to potentially interested readers, as well as make myself take a look at more ideas.

The level of depth will vary and some are outside my typical wheelhouse, so I may make mistakes. Feel free to bring them to my attention or ask questions and I’ll do my best to answer. I’ll try to do a few of these types of articles, so feel free to subscribe so you get emailed. Cheers

$STKS:

Overview:

STKS or One Group Holdings is the parent company of a handful of restaurant brands. You can likely guess what type of restaurant, so kudos to management on that.

The current brands under their umbrella include:

Benihana - The iconic Teppanyaki chain focused on Japanese food (but fun)

STK - Think steakhouse but Instagramified - vibe dining, not fine dining

Kona Grill - Imagine a Casino steak/sushi/American restaurant, but in strip malls

Ra Sushi - The chain version of a higher end roll based sushi restaurant

Assorted casino/hotel based one-shot restaurant concepts

Benihana and Ra Sushi were recently acquired in a debt funded acquisition in May, effectively a merger as the two companies were about the same size.

The overarching theme here is basically to take a popular food item, then dress it up with alcohol/music/showmanship to differentiate and grab higher margin. In theory this should fit into a social media culture pretty well.

Investment Hypothesis:

Acquiring a company with equivalent revenue and a similar margin profile isn’t particularly cheap, especially when it’s restaurants.

Basically we tossed in $350m of term note and $150m of prefs. The blended APR is something like 14%, so ~$70m of interest expense per year.

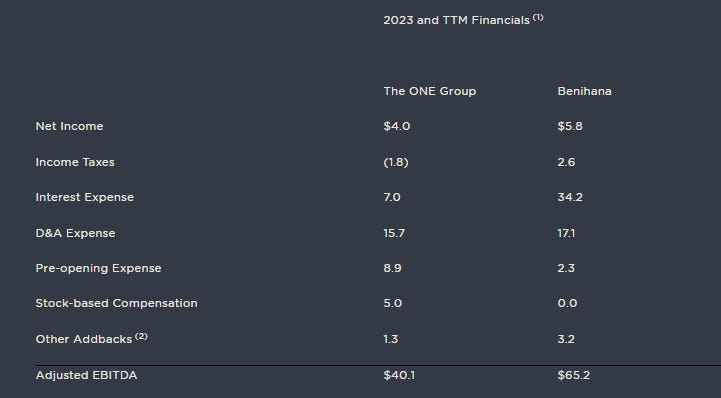

EBITDA looks roughly as follows

So $105m 2023 EBITDA, $70m interest expense added. Guidance for 2024 is $95-100m of EBITDA.

In terms of actual cash, CapEx likely should be >D&A (might not be, you just pay for it with topline), call it $25m for each. Pre-opening expenses are quite real as well. As a result cash change is probably something like $100m EBITDA - $70m int expense - $50m CapEx - $10m pre-opening = -$30m cash generation. Cash balance is $50m so near term liquidity isn’t an imminent concern.

Market cap is $131m.

So the basic idea is you have an extremely levered company betting it can realize synergies, improve cash generation via high ROIC new openings, and improve existing restaurant margins/performance. In such a case they would ideally start generating cash, refinance debt which generates more cash, etc. You get the virtuous cycle benefits of going from levered and ugly to less levered and less ugly.

As an example, consolidated revenue guidance is somewhere in the range of $700m-$740m. Adding 5% operating margin to that turns your ~$30m burn into ~$5m cash generation!

At that point the company can start exploring buying back debt/refinancing debt. Each 2% they could take off that 14% on $500m is $10m/$130m market cap. $350m of that debt is also floating based on SOFR, so any rate cuts are $1m each. Every $15m or so they take off the debt load is also $2m of savings.

So we could get something like the following:

Improve operating margins by ~5%: +$35m

Buy back $15m of debt: +$2m

1 rate cuts by YE 2024: +$1m

Add some new restaurants: +$10m

Net result is going from ~$30m burn to ~$20m cash generation vs $130m market cap in 2025.

Lots of assumptions baked into that and it’s more complicated than I lay out, but the idea is the company likely re-rates meaningfully higher. Even 10x FCF is ~40-50% higher stock price.

My thoughts:

I’m being very very surface level with the mechanics of the debt and their ability to improve core operations. The point is that it’s a very murky extremely levered situation where minor shifts can produce extreme outcomes to the up or downside.

To actually make an investment decision one would need to hammer down the exact mechanics of the debt (APR’s change each year, buybacks have terms, etc). You would also need to hammer out how much cash will be generated by new openings, how much will be burnt on pre-opening, and how the existing cohorts perform. The debt side of that isn’t particularly hard (simply boring), the fundamentals are a bit trickier.

These types of situations can be very difficult as management is fully incentivized to lie to you. A higher stock price provides a liquidity cushion and the #1 management incentive is to not blow up and lose your job. Building out the business performance and where/how they improve margins is quite difficult. Management has an information advantage and can selectively shed light on metrics they believe to be favorable, which makes things hard. The fundamentals are also the most important driver, so if you get them wrong you lose all your money!

At the same time, management opted into drastically levering up their company, so some credit has to be given to the fact they think they can make it work. Insiders aren’t always correct, but this isn’t a case of misfortune leading to debt, it’s an active transformational choice.

The company unfortunately doesn’t have a long track record of M&A activity, and the one acquisition thus far has been of middling success. Kona was purchased for $25m in 2019 and is currently generating ~$2m of restaurant level operating profits, probably making it breakeven or loss making in total. Now of course Covid happened and we’re currently in a bit of a tough spot for those types of restaurants, but clearly making restaurant chains profitable isn’t an easy endeavor.

I do believe the STK concept has done quite well and is by all accounts decently profitable with room for growth. Benihana is a classic and Asian food I do believe is on a cultural come-up, so I’d imagine there is room to improve. By no means are they in an impossible spot, simply a tricky one.

Personally I’d like to wait for more information from management regarding synergies and plans to improve operations in a more direct way. We don’t have good info on line by line financials for Benihana’s given the acquisition was mid Q2 and the info thus far is quite vague on how they will combine and leverage Benihana’s. Certainly an interesting situation to follow given all of the leverage, and would encourage interested readers to give it a spin if they think they can form a convicted opinion either which way.

$HOOD:

Overview:

I’ve tweeted a few times recently about HOOD, largely due to their recent promotions such as 3% IRA transfer match, 1% brokerage match, a 3% cashback credit card, etc. The basic premise for Robinhood is to have a brokerage focused less on fee capture/selling overpriced money management and more on gamifying the experience with a good UI for younger audiences. They were the guys who pioneered no fee stock and option trading, instead opting to monetize via Payment For Order Flow (PFOF).

We could get quite technical on how HOOD makes money, but the basic idea is that all the other brokerages are awful at making a UI and charge for things, so young users flock to HOOD. The average user has ~$5,600 in the platform as of May, which I’m quite sure is a function of users age. While having a brokerage catered to younger users can be interesting in the sense of locking them into a platform as they age and assets grow, I believe HOOD as another important driver.

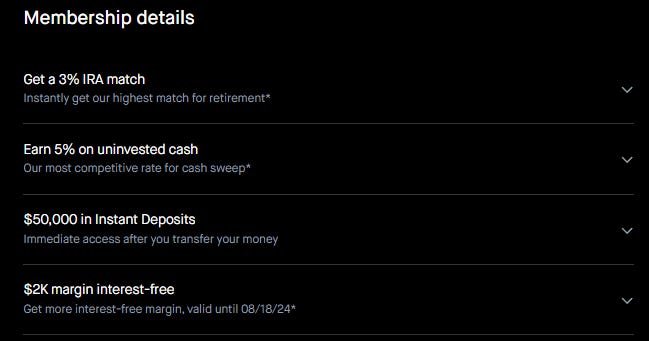

Lately they’ve been heavily pushing their Gold program. Essentially you pay $5 a month for the following list of perks:

In addition to these perks, they have been running promotional campaigns this year as previously mentioned such as the 3% IRA transfer match and 1% match on any deposit/transfer.

This is rather insane value. $2,000 interest free margin could simply be tossed into SGOV and yield more than the membership fee. For younger users contributing to an IRA a 3% match can be worth ~$200 annually. Promotions such as the 3% IRA transfer match were extremely popular and I myself transferred my smaller Schwab IRA to Robinhood and paid for more than a couple decades of Gold with that transfer. I facilitated a couple $1m+ account transfers that received more in transfer funds than they could conceivably pay for gold in a life time.

The obvious goal here seems to be trying to shift Robinhood perception to that of a more serious brokerage via attracting larger accounts. The promotion even got my 70 year old mother to swap to Robinhood. The UI is so simple and fluid she figured out how to trade like she was on Schwab within the day of transfer completion, quite the testament.

Product wise it’s quite phenomenal, albeit still lacking a few key features to justify putting a large primary account into it, such as lot selling for tax management and other such smaller needs. Assets Under Custody and funded customer metrics have been consistently growing and accelerating recently with the product improvements and value from Gold, so it’s hard to see how Robinhood doesn’t continue taking share of the brokerage market.

Investment Case:

The stock has run up quite substantially in the past year, +130% or so depending on the day. The current market cap sits right around $20b, however the EV is ~$15b.

From a current financials basis this undoubtedly looks quite expensive. TTM revenue sits at ~$2b with no GAAP earnings to speak of. This is largely due to some 1 shot accounting quirks last year that we are now lapping. Earnings in Q1 were ~$160m with revenue of $618m growing 40% YoY, so trailing numbers aren’t a great read and growth has been phenomenal, with the company trading at maybe ~33x 2024 earnings while growing topline ~40%.

Those numbers look far more attractive and can justify some serious attention.

My thoughts:

Brokerages do not work like traditional businesses, especially when much of your revenue is based on transaction revenue (53%). Robinhood basically monetizes based on a function of how often customers trade combined with how much they trade. The significant bull market in equities and crypto over the past year and half or so has been very beneficial to them. 40% YoY growth is not something they necessarily have much control over and could reverse course quite quickly if we saw adverse conditions in US equity markets or crypto markets.

Additionally, this is a business currently running what is effectively a science experiment with their marketing dollars. Paying users tens of thousands of dollars to transfer significant retirement assets en masse as well as their other customer buying endeavors are quite bold. Their last bet on PFOF in exchange for no fees worked out quite well, but I struggle to see how paying 3% for assets is going to be high ROIC unless there are beneficial second order effects beyond just the customer additions. I would give management more credit than say STKS above given their track record, but at ~30-35x earnings the room for error isn’t very wide in terms of attractive stock returns.

I do strongly believe in the product and wouldn’t be surprised if they can create quite sticky users due to far better tech and consumer offerings. AUC would then hopefully grow over time as you continue taking share with younger users and older cohorts age into higher net worth.

The timing and lumpiness of growth is the real question. To gain confidence in Robinhood’s continued significant growth would require confidence in overall market performance, a notoriously difficult task. I believe the 30-35x current valuation isn’t necessarily attractive if I’m taking that risk compared to other holdings of mine that are very sensitive to economic conditions like CVNA. I was an owner of HOOD at $10 last year and would be happy to take a more serious look back in the teens.

Regardless of my personal view however, I wouldn’t be surprised if Robinhood continues to do well as a business and the level of product differentiation makes it certainly worth consideration given it exists within a space where competitors hold hundreds of billions in market cap and seems to be out executing in many areas.

$NTES:

This one is a Chinese ADR, so if you hate those feel free to skip. The premise is pretty simple, they largely act as video game development company for external IP. This has a twofold benefit:

Video games are very broad in terms of story telling capabilities while having a very large potential audience base, so turning existing IP into a video game can be win/win for the IP holder and the game developer.

American video game publishers cannot publish their games in China directly and must enlist partners to do so.

As a result, NetEase has done quite well historically and is the 2nd largest game publisher in China behind Tencent. They focus primarily on mobile games which have significantly shorter development times and lower capital outlay while also being quite popular with domestic audiences.

The revenue is also somewhat globally diversified given they partner with popular western IP to produce mobile adaptations. Some examples:

Activision Blizzard: Diablo mobile game

Lord of the Rings mobile game

A couple Marvel mobile games

A Tom and Jerry mobile game (yes, the cat and mouse cartoon)

A Harry Potter mobile game

While this type of development typically leads to lower upside given they aren’t producing the IP, it’s more capital efficient and consistent due to leveraging existing audience bases. They do have organic IP as well, so it’s quite a diversified portfolio. (The organic IP makes up the majority of earnings due to higher margins).

They also manage all Blizzard titles in China, as well as Minecraft. The Blizzard agreement was actually exited a bit over a year ago due to disagreements on terms, then renewed once again. This alone should provide an >5% revenue boost over the next 12 months and all they have to do is publish already existing content.

Overall, it’s a very diverse player in a space that is quite strong both domestically and abroad. It’s more likely than not that IP continues being adapted to video game format, especially mobile, and if you work with a Chinese partner they can handle Chinese publishing for you as well due to our silly acceptance of Chinese trade laws.

Investment Case:

The ADR has an implied market cap of $62b which is about 15x earnings. Earnings have doubled or so in the past 3 years while revenue is up ~50%, largely driven by improved margins from continued execution on the mobile gaming side domestically with internal IP and international expansion of their existing titles.

Growth has slowed a touch due to industry wide post-Covid slowdowns, but is still robust with Q1 coming in at +7% for revenue and +14% for gross profit. Revenue growth should start accelerating in the 2nd half of the year due to renewal of a Blizzard publishing agreement, while also being somewhat accretive to the bottom line.

They’ve additionally done quite a few investments in the past couple of years into international gaming studios (smaller ones looking to develop titles primarily for Western audiences, similar to Tencent’s stakes in many Western developers). These projects are largely pre-revenue currently, which should be a boon over the coming years to diversify their portfolio and be earnings accretive.

Essentially a company with secular tailwinds due to expanding digital entertainment markets, trading for 15x earnings while growing 5-15%, with very sticky IP historically.

My thoughts:

Clearly there is an ADR/China video game discount here. I personally don’t particularly believe either of those will be a headache for me, but the possibility is of course non-zero.

Public high quality video game companies are very hard to find and we just saw MSFT gobble up ATVI. The western ones have largely been acquired besides EA and TTWO. Zynga is perhaps the best comparable to NTES in terms of portfolio and was acquired for ~5x revenue in 2022. ATVI had a very similar margin profile to NTES and was acquired for ~8x revenue. NTES by comparison trades for ~4x with a far better portfolio than Zynga and without the IP decline of ATVI. TTWO trades for >5x with a far worse margin profile as well.

As a result it really depends what questions you’d like to answer. If NTES was Western it would without a doubt be undervalued, so if you don’t think China is going to crackdown on gaming/western investment its a good bet on that front alone.

Even if you do, then playing for growth is always a worthwhile possibility. I’m quite bullish on these types of companies for a few reasons:

Generative AI is extremely useful for international video game publishers.

Translation and localization costs go down and times speed up. It can take years to localize games and millions of dollars. Having faster releases makes a big difference for a medium where visuals matter and costs go down.

Due to the exceptionally wide portfolio of NTES, models can be trained on internal art/models/etc to speed up workflows and should drive longer term efficiencies in operating expense.

Studio investments have become quite popular. Occasionally you hit a home run. TCEHY has Riot Games which is likely a 10x or more for them. These projects diversify revenue streams internationally and also lock-in the stakeholder as the Chinese publisher.

Mobile games being popular isn’t new per se in the West, but the Chinese market is far ahead in adoption. NetEase is a premiere mobile developer in China that is continuously improving international operations and has launched a couple western titles with millions of players. Simply opening up internationally is a relatively cheap growth vector.

Partner content will likely continue to accrue to higher tier developers such as NTES.

The much more frequent development cycles provide much more room for iteration than public Western developers focused on AAA console markets with significant capital outlays and uncertain returns.

Overall I’m quite positive on NTES. In-depth analysis is a pain given the Chinese aspect, however it’s likely hard to own in size regardless due to geographic concerns. This isn’t a near term catalyst play, more of a company with a great growth track record with a bright compounding future ahead (barring any governmental issues).

I do own NTES currently (but rather small), so take that as you will.

Conclusion:

Hopefully the short run throughs on these 3 tickers were helpful or at least interesting. I’ll do a couple more of these similar articles as I work through ideas forwarded to me and ideas I come across.

Cheers and hopefully we enjoy Q3.

I'd be interested in seeing your take on REAL. Debt overhang possibly diminishing under new leadership and business model shift.

just a feedback, I like the format a lot (even If I don't like these specific picks)